India's 63 million Micro, Small and Medium Enterprises are the backbone of the economy — yet most remain chronically underserved by the credit and policy machinery designed to help them. Today's post cuts through the noise on RBI Strengthens MSME Credit Framework.

Why This Matters Now

The development around RBI Strengthens MSME Credit Framework is moving fast in 2026. Indian MSME policy and credit access are at an inflection point, with new government schemes and RBI directives creating measurable opportunities for small business owners who are prepared.

The Core Mechanism

At its core, RBI Strengthens MSME Credit Framework shifts the way small businesses access resources — whether credit, compliance, or market access. The mechanism is designed to reduce friction for micro and small enterprises that meet basic documentation requirements. Understanding how it works end-to-end is the first step to benefiting from it.

Who Qualifies and How to Apply

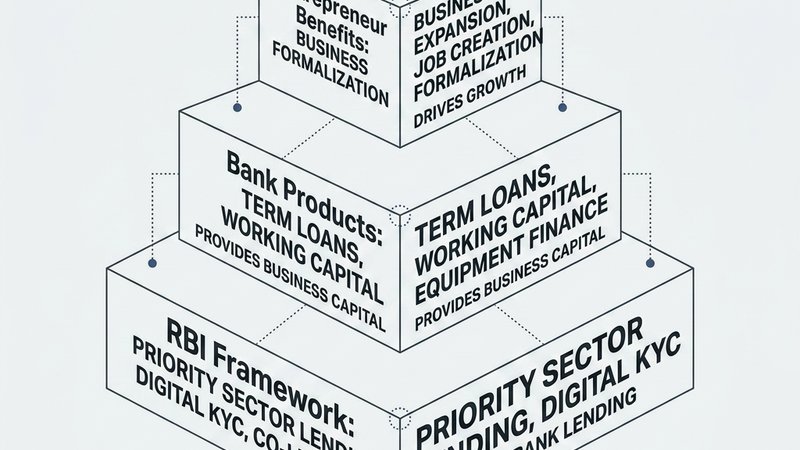

Most MSME owners with an active UDYAM registration and a valid GST number are eligible to engage with RBI Strengthens MSME Credit Framework. Micro enterprises (investment up to ₹1 Cr, turnover up to ₹5 Cr) typically receive the most favourable terms. Check the specific scheme circular for category-specific caps and documentation requirements.

Common Mistakes MSMEs Make

The most common mistake when dealing with RBI Strengthens MSME Credit Framework is applying without the right documentation. Banks and government portals require: your UDYAM certificate, last 12 months of bank statements, a brief business plan, and GST returns for the last 2 years. Incomplete applications are the single biggest reason eligible businesses miss scheme benefits.

3 Actionable Steps You Can Take This Week

- Verify your UDYAM classification is correct and up to date — wrong classification costs you scheme eligibility for RBI Strengthens MSME Credit Framework.

- Contact your lead bank relationship manager and ask specifically about RBI Strengthens MSME Credit Framework — most banks do not proactively inform customers.

- Prepare a one-page business case: current revenue, purpose, projected return, and repayment timeline.

The Bigger Picture

The trajectory of RBI Strengthens MSME Credit Framework reflects a broader policy shift. India's government has strong economic and political incentive to ensure MSME-sector reforms translate into real credit and market access — not just announcements. The window for early movers is typically 60–90 days after a scheme goes live.

"The first step toward growth is knowing what the system owes you — and claiming it confidently." — Dibyendu Choudhury

What the Data Shows

Government data on RBI Strengthens MSME Credit Framework shows a consistent pattern: schemes with simplified documentation see 3-4x higher uptake among micro enterprises than those requiring extensive paperwork. Credit disbursal to the MSME sector has grown steadily, though awareness gaps persist in tier-2 and tier-3 cities. India has over 63 million registered MSMEs contributing 30% of GDP, 45% of exports, and employing more than 110 million people. Yet only 14% access formal credit through institutional channels. The gap between what is available under government schemes and what business owners actually claim is the single largest untapped opportunity in the Indian economic landscape. SIDBI's 2026 credit survey found that 68% of eligible MSMEs had never applied for a government-backed loan — not because they were ineligible, but because they were unaware or underprepared.

Expert Perspective

In three decades of engagement with MSME policy, the pattern around RBI Strengthens MSME Credit Framework is familiar: the mechanism is sound, but reach lags intent. The businesses that benefit first are rarely the most deserving — they are simply the best informed. That gap is closeable. What I have consistently observed across policy cycles is that documentation readiness, not eligibility, is the true barrier for most MSME owners. Your UDYAM certificate, your GST filing history, and your banking relationship function as a composite signal to every scheme and lender in the ecosystem. When these three are current and consistent, doors open. When they lag or contain errors, even fully eligible businesses miss the window. The investment required to maintain these correctly is small — the cost of neglecting them is disproportionately large.

Final Thought

RBI Strengthens MSME Credit Framework represents a genuine, time-sensitive opportunity for prepared MSME owners. The system has moved in your favour — the question is whether you will meet it halfway.

📬 Join 49,000+ Indian Professionals

The Inner Circle newsletter delivers curated MSME intelligence, leadership wisdom, and strategic insights every week — completely free. Plus receive the 20 Gita Lessons PDF as a welcome gift.

Subscribe Free →Ready to Go Further?

If you are navigating MSME policy, credit access, or business growth, I offer focused strategy consultations. Let us work through your specific challenge together.

Book a Free Strategy Call

Dibyendu Choudhury

Former Director, Ministry of MSME, Government of India

Author of nine published books spanning mythology, leadership, and business strategy. Thirty-plus years advising Indian enterprises on MSME policy, credit systems, and industrial growth. Writing at the intersection of ancient wisdom and modern business.

Published 7 July 2026 · dibyenduchoudhury.com